June — a month of two extremes. What does the market actually pay energy‑storage units for?

In a single month, the Polish power system showed energy‑storage operators both faces of the future. At midday, surplus solar generation pushed prices below zero, while in the evening of 30 June – on a capacity‑call day – day‑ahead (DA) market prices exceeded 2,000 PLN/MWh. The flexibility premium shifted between these extremes.

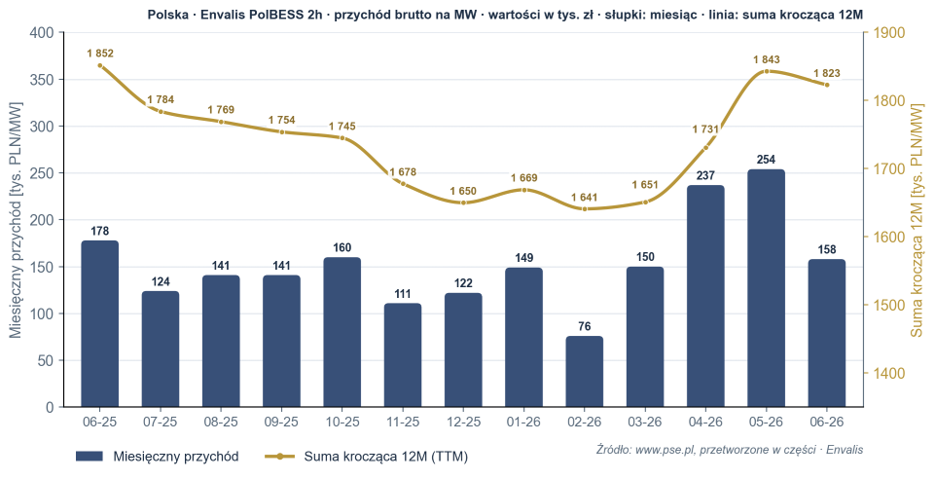

A two‑hour reference storage unit (1 MW / 2 MWh) earned 1,823,360 PLN gross per MW of power over the past 12 months, with June alone contributing 158,299 PLN.

Methodology. Envalis PolBESS is a historical, monthly benchmark of gross revenue for a reference storage unit (1 MW / 2 MWh) in the Polish market, calculated by the Sentinel engine using real market data. It is not a forecast or a valuation of any specific project. Full methodology: www.envalis.energy.

Readiness still rules

Where does this revenue come from? Still primarily from remuneration for readiness to provide system services — that is, keeping the storage unit in a state that allows it to respond in the required direction. This component accounted for most of June’s result.

However, the storage unit also earns revenue when it is actually activated. Activation energy had a noticeable share in June, and its importance is gradually increasing. Classic day‑ahead arbitrage performed by far the weakest. Spring price flattening made its contribution to the June result almost zero.

The conclusion remains unchanged: almost all storage revenue still relies on system services, and within them primarily on readiness remuneration. This is both the greatest strength and the greatest weakness of the current business model.

It is worth distinguishing between the two directions of readiness. Up‑regulation means the obligation to deliver energy when the system lacks it. Down‑regulation means readiness to absorb surplus energy. It is the shift in the relationship between these two products that best explains June’s events.

A weaker month, but not a weaker market

June’s result was more than 30% lower than the 254k PLN achieved in May and 237k PLN in April. However, this does not indicate market deterioration. It is rather a recurring spring oversupply phase, when the system has the highest solar and wind generation while demand is near its annual minimum.

Importantly, despite the weaker month, annual earning capacity has barely changed. The rolling 12‑month result fell only from 1.843 million PLN to 1.823 million PLN per MW, remaining very close to the yearly peak reached in May.

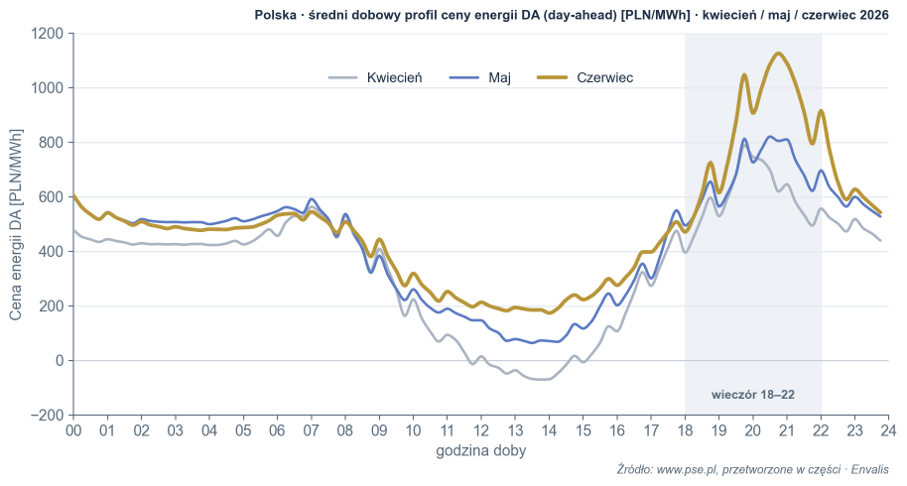

This is most clearly visible in the daily price profile. The duck curve is becoming increasingly steep. The average midday price rebounded from the April minimum — from -15 PLN/MWh in April, to 110 PLN/MWh in May, and 203 PLN/MWh in June. Evening “neck” prices rose even faster: 601, 682, and 845 PLN/MWh respectively. As a result, June delivered the largest gap yet between the midday trough and the evening peak.

The premium has changed direction

Day‑ahead market prices show where tension in the system is building, but in the PolBESS benchmark the storage unit captures most of its value not through energy arbitrage, but through the provision of system services. And that is precisely where the shift is most visible.

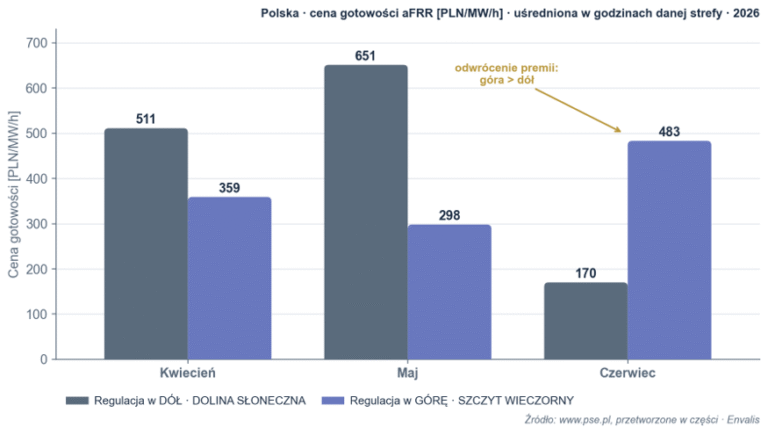

In spring, the highest‑priced service was down‑regulation readiness during the Solar Valley hours — the period of peak PV generation. In April it stood at 511 PLN/MW/h, rising to 651 PLN/MW/h in May. During the hours of maximum solar output, the ability to absorb surplus energy was simply the most valuable service.

At the same time, up‑regulation readiness during the Evening Peak was priced significantly lower — 359 and 298 PLN/MW/h, respectively.

June reversed this relationship. The price of down‑regulation readiness in the Solar Valley fell to 170 PLN/MW/h, while up‑regulation readiness in the Evening Peak rose to 483 PLN/MW/h. For the first time since spring, the evening ability to deliver energy became the most valuable service.

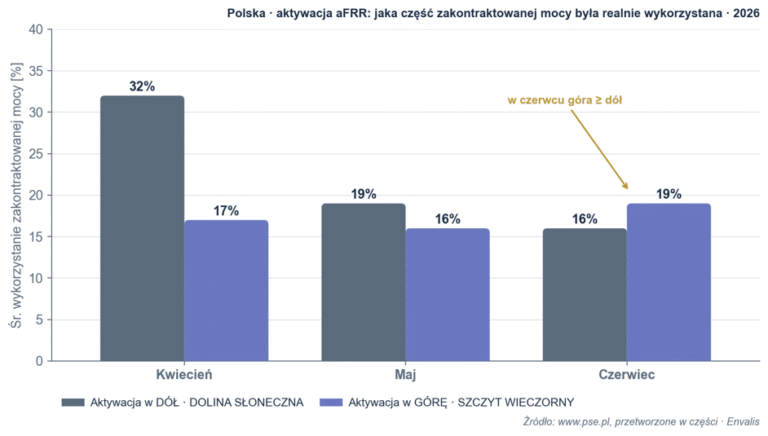

The data on actual storage activation confirms this as well. In spring, the operator most frequently used storage units to absorb surplus energy in the middle of the day. In the following weeks, the number of such activations decreased, while calls to deliver energy in the evening became increasingly common. The direction of actual storage operation shifted in exactly the same way as the valuation of readiness.

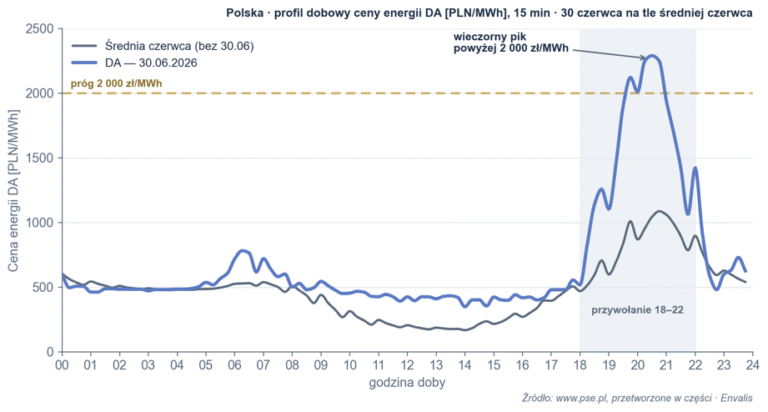

The evening that revealed the future

On 30 June, during a heatwave, PSE activated the capacity‑call mechanism for the third time in history, obliging units holding capacity contracts to make their power available to the operator. This applied to the hours between 18:00 and 22:00, when solar generation had fallen practically to zero and demand — driven by air conditioning — remained high.

The situation was further worsened by outages at Kozienice (200 MW) and Turów (444 MW) as well as weak wind generation. The reserve shortfall reached 400–800 MW, and day‑ahead market prices exceeded 2,000 PLN/MWh during those hours — more than four times the average for a typical June day, which is around 480 PLN/MWh.

It is worth separating two mechanisms. The capacity‑call procedure concerns the capacity market, a distinct instrument based on capacity contracts. Meanwhile, the revenues included in the benchmark come from balancing services (aFRR). That evening, the capacity market served primarily as a signal of rising system stress, not as a direct source of storage‑unit revenue.

This is only the beginning of the shift

These two faces of a single month — midday PV oversupply and the evening shortage pushing prices above 2,000 PLN/MWh — illustrate why the flexibility premium has shifted from down‑regulation to up‑regulation.

This does not mean that storage units stopped charging and began exclusively discharging. The operating cycle remains the same. What has changed is the direction for which the system pays the highest remuneration. In spring, the most valued capability was absorbing surplus energy in the middle of the day. In June, the most valuable capability became readiness to deliver energy in the evening.

Crucially, this is not classic energy arbitrage. Storage captures this value primarily through the provision of system services. The system pays not for buying energy cheaply and selling it at a higher price, but for readiness to respond exactly when that response is most needed. This is why storage duration and evening availability are becoming increasingly important — they determine how much value can be offered in the most sought‑after direction of regulation.

There is, however, another side to the coin. Today, almost all revenue comes from a single source. This is comfortable now, but in the future it will become a risk. As the number of storage units grows, readiness prices will gradually decline, and the revenue burden will shift toward activation and energy arbitrage.

Today’s high storage revenues in Poland are not a durable competitive advantage. They are primarily a consequence of low system flexibility and the still small number of operating batteries. As more projects come online, service prices will converge toward levels observed in more mature markets. Those who will succeed are the ones already building business models based on multiple revenue streams, not solely on readiness remuneration.

June turned out to be a miniature version of the market we are heading toward. In a system with a growing share of renewables, the scarce resource is not energy but flexibility — and storage is its purest form.

Because in the energy system of tomorrow, the winner will not be the one who has the most energy, but the one who can deliver it exactly when it is needed most.

Jacek Janiuk, CIIA

Founder and CEO of Envalis, a consultancy specializing in the valuation and risk assessment of energy storage systems and hybrid RES+BESS projects. He has over 25 years of experience in investment, management, and finance. His past roles include President of Pekao TFI, Head of the Investment Advisory Department at Citi Handlowy, and Head of the Brokerage House at Alior Bank. He combines capital market expertise with a technical understanding of the power system. At Envalis, he is responsible for methodology, risk models, and benchmarks for energy storage assets.