The story of one hot evening. The third capacity‑call event in PSE’s history, and balancing energy remained inexpensive.

June 30, 2026: Poland’s grid operator reached for a tool it had used only twice before in its entire history.

It was a kind of alarm — a formal signal that in the next several hours the system might run short of capacity. The day‑ahead market had already warned of an approaching crisis the day before: prices had shot upward. And yet, when that evening actually arrived, energy did not become expensive where real‑time balancing is paid for. The alarm sounded, and something happened that the price panic had not predicted. What exactly happened — and who was behind it — becomes clear only at the end of this story.

This puzzle is the most important lesson of the entire hot June. To understand it, we traced three days, quarter‑hour by quarter‑hour, using PSE data with 15‑minute resolution. And to understand it, one must begin not on June 30, but two days earlier.

Let’s go back two days: a heat dome and dead wind

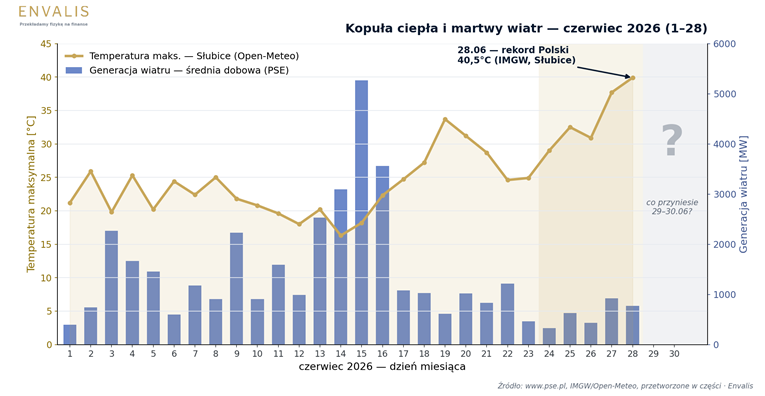

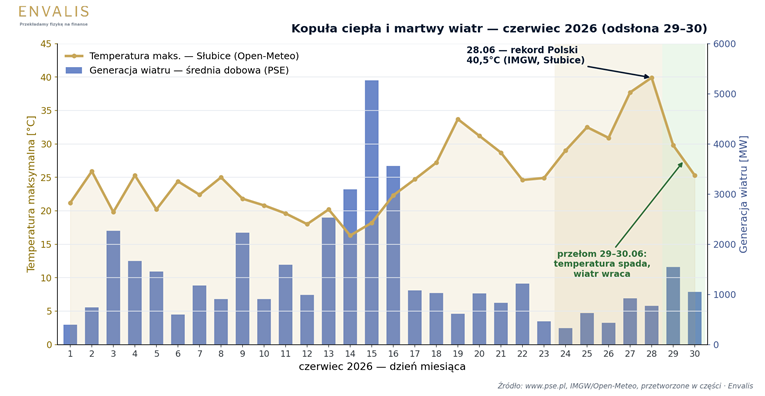

Tension in the system — just like panic on the market — does not appear suddenly. It builds. It was late June, and a vast “heat dome” slid over Europe, a high‑pressure system that pushed temperatures 14–18°C above normal day after day, giving Western Europe the hottest June in the history of measurements (+3.05°C vs. the 1991–2020 norm). On June 28, records fell on both sides of the Oder: 41.7°C in Coschen, Germany (the all‑time German record), and 40.5°C in Słubice (the highest temperature ever recorded in Poland, according to IMGW‑PIB).

Such weather is a double blow to the power system. On one hand, millions of air conditioners run at full capacity and do not switch off after sunset because hot nights bring no relief. On the other hand, the same heat dome that warms Europe simultaneously puts the wind to sleep. Germany recorded its lowest weekly wind generation of the entire year in the week ending June 28. Poland was identical: wind output on June 28 fell to 203 MW, despite several gigawatts of installed capacity. At the very moment when cooling demand was at its peak, one major renewable source disappeared from the balance almost entirely.

France shuts down nuclear capacity, the import buffer disappears

At the same time, France’s nuclear fleet was falling out of Europe’s supply. The heat warmed the rivers that cool the reactors — the Seine at the Nogent plant, the Rhône at Bugey, and the Garonne at Golfech — beyond thresholds at which the law requires limiting the discharge of warm water. EDF shut down around 6.2 GW of nuclear capacity, nearly 10 percent of its fleet. To illustrate the scale: this is more than the capacity of Poland’s largest power plant, Bełchatów, meaning the equivalent of roughly six large nuclear units taken offline at once.

The effect was immediate across Europe. French exports fell from 10–12 GW to around 3 GW, French spot prices rose to their highest levels since January 2025, and at the peak the continent recorded levels unseen since the 2022 crisis (in Belgium, on June 24, the price briefly exceeded €1,000/MWh). For Poland, this meant one thing: the cheap imports that normally cushion the evening peak were disappearing. The buffer the system usually relies on after sunset was closing — and the sharpest impact was expected on June 30, when the evening cross‑border exchange balance fell almost to zero.

The heart of the problem: residual load

The entire mechanics of these three days fit into a single curve: residual load, meaning demand minus generation from solar PV and wind. This is the power that the rest of the system must cover — thermal units, pumped‑storage plants, batteries, and imports. When the sun shines, residual load drops almost to zero. When it fades, everything else must instantly take its place.

A quarter century ago, the seasonal load profile of a single transformer station was enough for me to write an engineering thesis in mathematics. Today, the same curve — stretched across the entire system and reported every 15 minutes — determines whether there will be enough power in the evening. Some questions return, only at a much larger scale.

Midday: PV floods the market

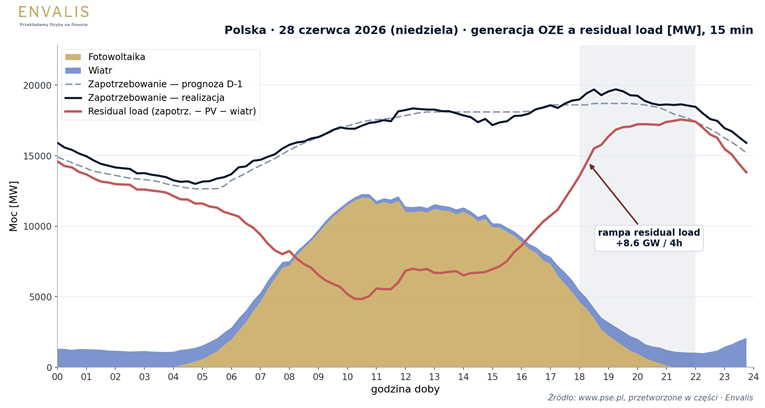

On June 28 (Sunday), solar PV reached 12 GW, residual load collapsed to 4,830 MW at 10:30, and PSE had to curtail PV, temporarily by as much as 2,475 MW, across 44 quarter‑hours of the day (June 2026 was record‑breaking: a total of 286.6 GWh of renewable energy was curtailed). The surplus was so large that Poland was exporting power at noon, and balancing‑market prices plunged deep below zero — to −2,484 PLN/MWh at 13:30.

Evening: the solar cliff

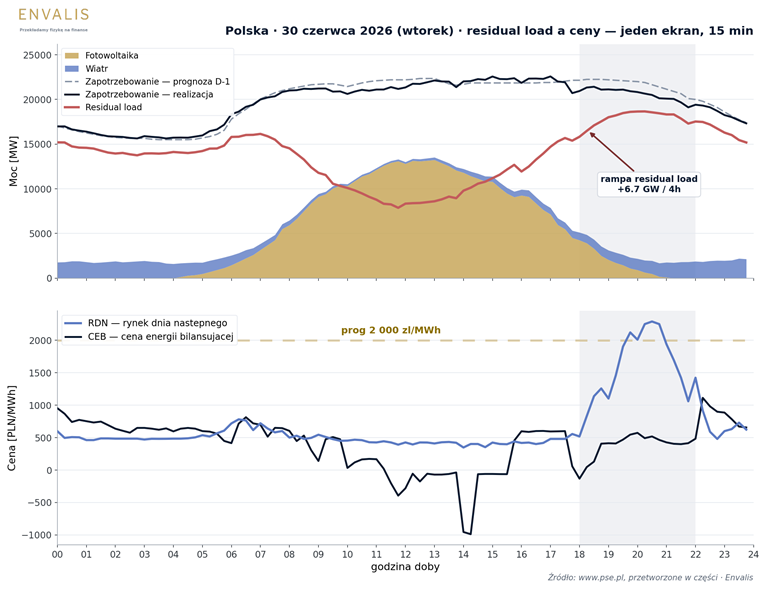

Then came the solar cliff. After 18:00, as PV faded and wind did not wake up, residual load shot upward — from the midday minimum of 4,830 MW to 17,562 MW in the evening. In the four‑hour evening ramp window alone, the increase reached 8.6 GW.

June 28: the thick “belly” of solar PV pushes residual load down to 4.8 GW at noon (negative prices, PV curtailment), only to shoot upward by 8.6 GW in four hours after the evening solar cliff.

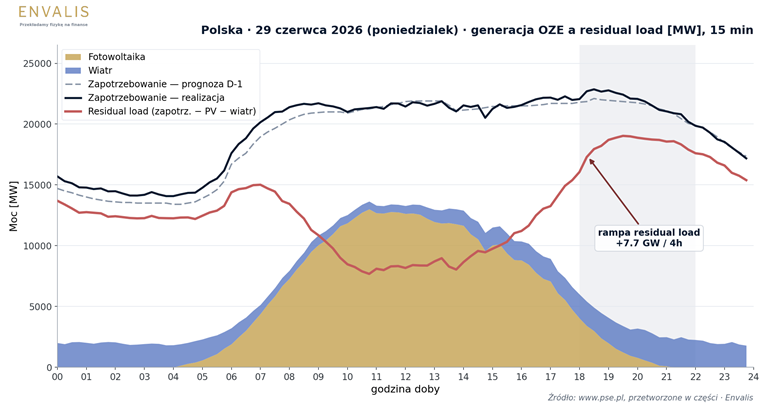

The same sequence is visible on each of the three days (a 6.7–8.6 GW ramp over 4 hours). This is no longer the “evening peak” known for decades. It is a wall the system must build in just a few hours.

Three days, three different market responses

Each of the three days responded differently, and the differences say more than the records themselves.

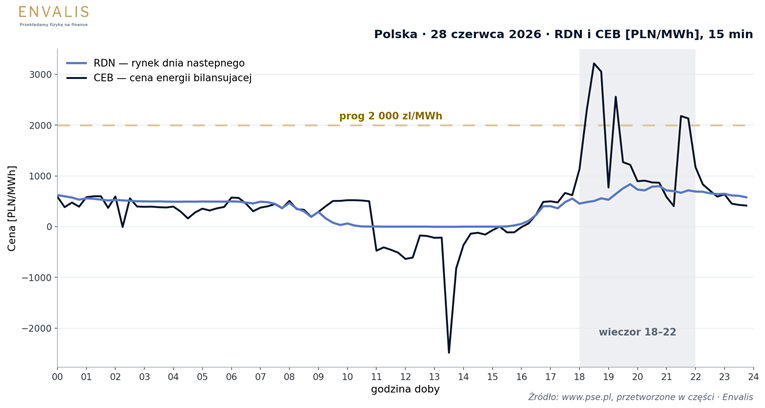

June 28 (Sunday): calm day‑ahead market, wild balancing market. Low weekend demand and maximum PV output produced a mild day‑ahead market (an average of 380 PLN/MWh), but the balancing market went crazy in both directions: from −2,484 PLN/MWh at noon to +3,215 PLN/MWh in the evening. All the tension shifted into balancing — a day when it was not the exchange, but the real system that took the hit.

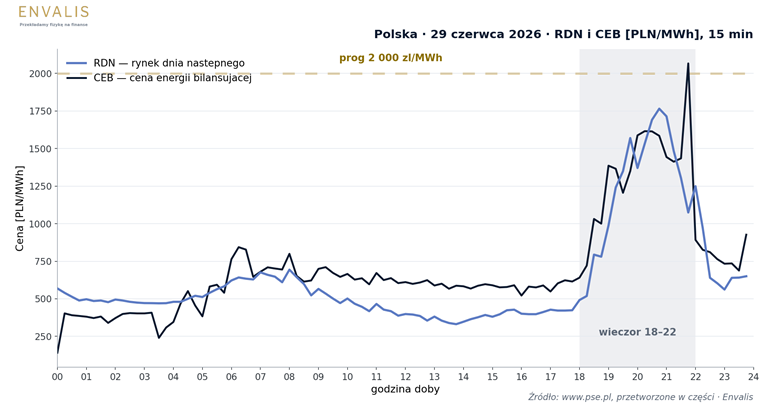

June 29 (Monday): “expensive together with Europe.” The return of full industrial and office demand (a peak of 22,858 MW at 18:30) combined with an expensive continental market pushed both indices upward in tandem: in the evening the day‑ahead market reached 1,229 PLN/MWh, and the balancing market 1,341 PLN/MWh, without a single negative quarter‑hour during the day.

When the exchange and the balancing market rise together — and rise high — it is a signal of a fundamental, not local, deficit.

June 30 (Tuesday): the day of the capacity call

Morning of June 30. Solar PV was only beginning to ramp up, and the operator was already looking not at what existed, but at what the evening would bring: rising demand driven by the heat, the sun that would begin to fade in a few hours, weak forecast wind, and closed imports. At 09:51, PSE issued a notice. For three evening hours — 18–19, 19–20, and 20–21 — it announced capacity‑call periods on the capacity market: a formal request for capacity‑market units to fulfill the obligation for which they receive remuneration. Generators must make capacity available or feed it into the grid, and DSR units must reduce consumption.

And then the situation deteriorated visibly. Wind generation crumbled throughout the morning: from 1,086 MW at 06:00 to just 187 MW at 11:00, the lowest level of the entire day — precisely during the hours when the operator was issuing and expanding the notice. Less than three hours after the first alarm, at 12:43, PSE issued a second notice and added a fourth hour, 21–22. On one of the hottest days in the history of Polish measurements, step by step, they expanded the alarm — not yet knowing how the evening would actually end.

The reason was stated plainly: “The need to announce capacity‑call periods results, among other factors, from high demand related to the heat, low forecast wind generation, and unavailability of capacity in conventional units.”

At that time, reduced capacity was coming from units at Kozienice, Turów, Ostrołęka, and Żerań — individually small outages, but collectively enough to deepen the reserve deficit.

A capacity call is a rarely used remedial measure of the capacity market, activated when forecast capacity surplus falls below a safe level; only load‑shedding stages are measures of last resort. Previously, PSE had announced capacity‑call periods only twice: 23 September 2022 (two hourly windows) and 6 November 2024 (three windows). June 30, 2026 was the third such day in the history of the capacity market — and the broadest, with four windows, and the first triggered by heat.

The market did not need a notice to sense the danger. Already the day before, in the day‑ahead auction for June 30 delivery, the evening price soared: in the 18–22 window it averaged 1,578 PLN/MWh, and at the peak at 20:30 it reached 2,290 PLN/MWh, more than four times the normal daily average. Everything pointed to a crisis.

What actually happened?

Then the evening came — and it turned out that the balancing‑energy price in those same critical hours averaged only 374 PLN/MWh. The CEB shows the settlement price of balancing energy once realization is known; it is not a measure of the total cost of securing the system, but it does show how expensive real‑time balancing was. It was lower than on an average weekday evening of the same month (around 900 PLN/MWh). The spread between the day‑ahead market and the balancing market reached nearly 1,800 PLN/MWh at the peak. The market had priced in panic the day before. Reality turned out calm.

Three things contributed to this — all on the system side.

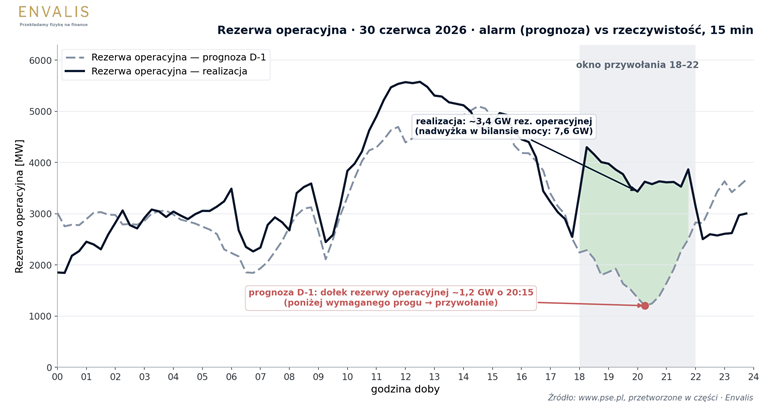

First, the alarm concerned the forecast, not the actual situation. The day‑ahead forecast of operational reserve collapsed in the evening to just 1.2 GW at 20:15, below the required level. That dip triggered the capacity call. But in real‑time operation, the operational reserve held at ~3.4 GW, and the surplus in the broader KSE capacity balance reached 7.6 GW — a margin the market feared, but which largely materialized.

Second, the wind woke up exactly when the sun went down. As solar PV collapsed within two hours from 4,250 MW (18:00) to 479 MW (20:30), wind generation increased: from 869 MW, through 1,265 MW (20:00), to 1,880 MW (22:00). The dead wind minimum occurred in the middle of the day, not during the peak. Two sources that can fail simultaneously on a hot evening this time joined forces.

Third, dispatchable units executed the ramp without breaking a sweat, increasing output by 5,333 MW between 14:00 and 20:00. During the evening peak, the realized operational reserve stood at around 3.4 GW, and the surplus of available capacity in the broader KSE balance reached roughly 7.6 GW. The system did not come close to the edge at any moment.

Two prices, two different truths

Here lies the essence — the point the market often loses. The day‑ahead market (RDN) and the balancing‑energy price (CEB) measure two different things. RDN is an ex‑ante price, shaped by participants’ expectations about the balance and by the pricing of risk associated with a difficult evening; an evening deficit with zero solar PV, weak wind, and no imports was fully plausible on D‑1, so the market bought insurance. CEB is an ex‑post settlement price, set once the actual system trajectory is known, when uncertainty has fallen on the favorable side. In this light, the reserve shortfall that triggered the capacity call and the comfortable ~3.4 GW of realized operational reserve (with a surplus of around 7.6 GW in the broader KSE capacity balance) are not a contradiction but two sides of the same story.

A capacity call is based on the forecast margin on D‑1/D‑2 — it is an ex‑ante signal. Realization is ex‑post. The operator’s task, through contracted reserve and unit scheduling, is precisely to ensure that the tail risk does not bite. On June 30, it worked.

A nuance is worth adding: marginal aFRR activations were expensive, with upward activation prices jumping above 1,700 PLN/MWh in the evening, but this was a thin slice at the top of the ramp. The bulk of the energy was delivered by scheduled units at normal cost. High marginal price, low average price — the signature of a well‑secured system.

Buy the rumor, sell the fact. And the Guardian who closed the system

What happened on June 30 follows a pattern perfectly familiar from financial markets: “buy the rumor, sell the fact.” The day‑ahead market priced the evening on the rumor — on fundamentals: heat, dead wind, fading French nuclear, and closed imports. It priced them earlier than the operator itself, because the RDN auction closed on June 29 in the afternoon, before PSE published the reserve forecast dropping to 1.2 GW, and before the morning capacity‑call announcement. The market did not trade the alarm; it traded the same fear that later produced the alarm. Hence prices above 2,000 PLN/MWh.

And when the facts arrived — realized reserve, milder weather, returning wind — the balancing‑energy price settled low. The spread between RDN and CEB, nearly 1,800 PLN/MWh at the peak, can be read as the gap between forecast pricing and realization: as information flows in, the intraday market and activation prices converge toward the imbalance price. How much of that spread is a risk premium, and how much stems from offer construction, unit constraints, or participants’ positions — the spread alone does not decide. But it was available to those who could capture it: those who had power to deliver exactly at 20:00.

These three days were not a harvest for storage; in raw numbers, June had better ones. But they showed something more important: where future advantage lies. The evening spread was enormous, but it does not collect itself. It will be captured not by whoever has the largest battery, but by whoever predicts best and decides fastest. And such evenings will only multiply, because as the share of renewables grows, volatility grows — and France’s example shows that even a nuclear fleet is not weather‑proof. Capacity alone stops being enough. What matters is forecasting, decision‑making, and readiness on both sides of the meter.

Above all this, someone else was watching. And who was behind it? Here the question from the beginning of the story returns. The answer is: the Guardian. In the strategy published on 16 December 2025, “The Guardian and the Architect. PSE Strategy to 2040,” the operator explicitly adopted two roles: the architect, who rebuilds the grid for a zero‑emission mix, and the guardian, whose task is the safe operation of the system here and now.On 30 June, we saw that guardian in action. PSE read the narrow reserve margin and, on the morning of June 30, reached for a tool used only twice before — a capacity‑call on the capacity market. They executed it precisely. The forecast reserve was missing only a small amount relative to the required level, not several gigawatts, so it was a targeted intervention, not an emergency measure. Capacity‑market units were called to make capacity available, and DSR units were obliged to reduce consumption.

And here lies the core. A capacity call is not measured by how much power was actually activated, but by how much stood ready in case the evening went the other way. This time the market helped, the weather eased, the wind returned, and the real deficit turned out small — so the Guardian needed little. But had the wind not woken up, had demand not fallen from the forecast, had another unit tripped, behind the capacity call stood the entire pool of contracted capacity, ready to enter the game.

The value was not in the energy used, but in the readiness for a scenario that did not materialize. This was not a slide‑deck declaration — it was strategy in action.

System security is measured not by how much power was activated, but by how much stood in reserve when the alarm sounded.

This analysis is based on public PSE data and market and weather data. What the market truly looked like — down to the megawatt and down to the decisions — is known in the PSE control room. This is an attempt to reconstruct and assess what happened, seen from the outside, through numbers.

Jacek Janiuk, CIIA

Founder and CEO of Envalis, an advisory firm specializing in the analysis, valuation, and bankability assessment of energy‑storage assets and hybrid RES+BESS projects. He has more than 25 years of experience in investments, risk management, and finance. Previously, he served as CEO of Pekao TFI, Head of the Investment Advisory Office at Citi Handlowy, and Head of the Brokerage Office at Alior Bank.

He combines capital‑market expertise with a technical understanding of the power system. At Envalis, he is responsible for methodology, risk models, and revenue benchmarks for energy‑storage assets.

Leave a Reply